Learn how federal student loan consolidation works, how to lower your monthly payments with IDR plans, and how Docupop simplifies the paperwork.

Are your wages being garnished? Learn how to get your federal student loans out of default through loan rehabilitation or consolidation and stop collections.

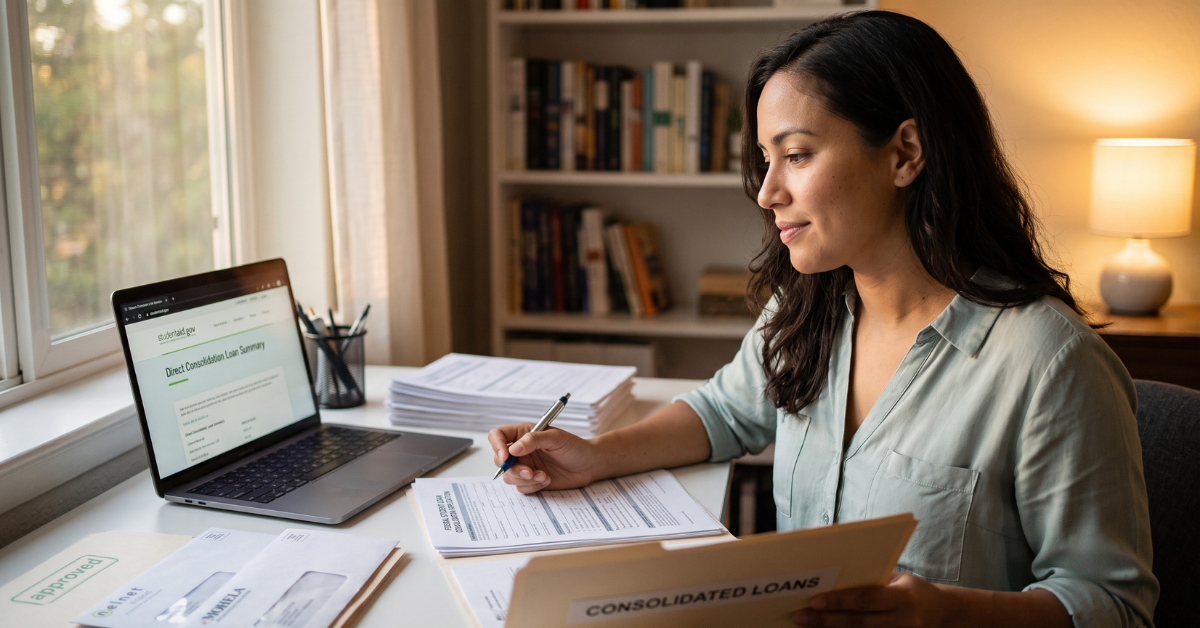

If you are managing multiple federal student loans, you have likely considered consolidation. Combining your loans into one Direct Consolidation Loan simplifies your monthly payments. It can also open the door to better repayment plans. But for borrowers who have been paying down their debt for years, a major fear holds them back. They worry that consolidating will erase their progress and restart their forgiveness clock back to zero. For a long time, that fear was entirely justified. Under old Department of Education rules, consolidating your loans meant creating a brand new loan. That new loan had a repayment count of zero, wiping out any progress you had made toward Income Driven Repayment (IDR) forgiveness or Public Service Loan Forgiveness (PSLF). Today, the rules have changed. The short answer is that consolidating your federal student loans no longer completely resets your forgiveness clock. However, the way the Department of Education calculates your past payments depends on specific timelines and new regulatory frameworks. Understanding exactly how your payment counts will be treated is critical before you submit a consolidation application. The Old Rules Versus The New Reality To understand where we are now, it helps to know the history. Prior to recent reforms, the Department of Education treated a Direct Consolidation Loan as a completely new financial instrument. If you had 60 qualifying payments on a loan and chose to consolidate it with another loan, the new consolidated loan would start at zero payments. This policy trapped many borrowers. If they needed to consolidate to access a more affordable payment plan or to bring older Perkins or FFEL Program loans into the Direct Loan program, they had to sacrifice years of hard earned progress. The Department of Education recognized this flaw and introduced temporary waivers, followed by permanent rule changes, to protect borrowers seeking relief. How Consolidation Affects Your Payment Count Today Currently, consolidating your federal student loans will not drop your payment count to zero. Instead, the Department of Education uses a weighted average approach to determine how many qualifying payments will be credited to your new Direct Consolidation Loan. Understanding the Weighted Average Rule Under the standard rules in effect today, your new consolidation loan will be credited with a weighted average of the qualifying payments made on the underlying loans. Here is how the weighted average works in practice. Suppose you have two federal student loans. Loan A has a balance of $20,000 and has 60 qualifying payments toward forgiveness. Loan B has a balance of $10,000 and has zero qualifying payments. If you consolidate these two loans, the Department of Education will look at the total balance, which is $30,000. They will then weigh the payments based on the proportion of the balances. Because Loan A makes up two thirds of the total balance, its 60 payments carry more weight. The resulting consolidation loan will not drop to zero, nor will it take the full 60 payments. It will land somewhere in the middle, reflecting the mathematical average of the loan histories. This means you do not lose all your progress. However, if you mix loans that have a long repayment history with brand new loans, the total payment count on the new consolidated loan will be lower than the count on your oldest loan. Consolidation and Public Service Loan Forgiveness The rules for Public Service Loan Forgiveness closely mirror the rules for IDR forgiveness when it comes to consolidation. If you are working toward PSLF, you know that you need 120 qualifying payments to receive tax-free forgiveness. If you consolidate your loans today, your PSLF payment count will also be subject to the weighted average rule. Borrowers pursuing PSLF need to evaluate their loan portfolios carefully. If all of your loans went into repayment at the exact same time and have the exact same number of qualifying payments, consolidating them will result in a weighted average that equals your current count. You lose nothing. However, if you have loans from undergraduate school with 80 qualifying payments and loans from graduate school with only 10 qualifying payments, consolidating them together will lower the count on your older loans while raising the count on your newer ones. You must calculate whether the convenience of a single loan outweighs the delay in forgiveness for your oldest balances. The Repayment Assistance Plan (RAP) and Tiered Standard Plan When determining whether or not you should consolidate, there is now a massive new consideration regarding recent regulatory changes. If you consolidate your loans after July 1, 2026, you will only be eligible for one of two repayment options: the Repayment Assistance Plan (RAP) or the Tiered Standard Plan. Crucially, Parent PLUS Loan borrowers who consolidate after that date are entirely ineligible for RAP. This means they would only be eligible for the Tiered Standard Plan, which offers absolutely zero loan forgiveness. If you hold Parent PLUS Loans, consolidating them under these new rules could permanently eliminate your path to forgiveness. Why Borrowers Still Choose to Consolidate Given the weighted average rule and the new repayment plan restrictions, you might wonder why a borrower would consolidate if it risks lowering the payment count on their oldest loans. There are several strategic reasons why consolidation remains a vital tool for federal student loan borrowers. Accessing Better Repayment Plans Not all federal loans are eligible for the most generous Income Driven Repayment plans. For example, older FFEL Program loans and Perkins loans do not typically qualify for certain favorable IDR plans unless they are consolidated into a Direct Consolidation Loan. Getting Out of Default If your loans are in default, you are locked out of forgiveness programs entirely. Consolidating defaulted federal student loans is one of the primary ways to return to good standing. Once in good standing, you can enroll in an IDR plan and start making progress toward forgiveness again. Simplifying Finances Managing five or ten different loan servicers and due dates is incredibly stressful. Consolidation leaves you with one monthly payment and one servicer, significantly reducing the mental burden of student debt. Common Mistakes to Avoid The consolidation process requires careful attention to detail. A simple mistake can cause delays or force you into a repayment plan you cannot afford. First, do not consolidate private student loans with federal student loans. If you refinance federal loans through a private bank, you strip away all federal protections, including access to IDR plans and PSLF. Second, make sure you select the correct repayment plan during the consolidation application process. If you consolidate but fail to enroll in an Income Driven Repayment plan, you may be placed on a Standard Repayment Plan. Payments made on the Standard Repayment Plan for consolidation loans do not always count toward PSLF. Third, understand the difference between joint spousal consolidation loans and individual loans. Congress recently passed legislation allowing borrowers to separate old joint spousal consolidation loans, but creating new ones is not an option. Keep your federal debt separate from your spouse to maximize your individual forgiveness timelines. Fourth, you may not want to consolidate Parent PLUS Loans together with non-Parent PLUS Loans. Any consolidation that includes a Parent PLUS Loan is ineligible for IDR plans, meaning you will lose out on loan forgiveness. Keep these loans separate to maintain your forgiveness progress on eligible loans. How Docupop Streamlines the Process Deciding whether to consolidate requires looking closely at your loan types, your current payment counts, and your long term career goals. Navigating the Department of Education websites, reading through pages of dense regulatory text, and filling out the applications correctly takes time and energy that most working professionals simply do not have. This is where Docupop steps in. We take the guesswork out of federal student loan document preparation. Our team understands the nuances of the weighted average rule. We help you review your current loan status, identify which loans are eligible for consolidation, and prepare the necessary paperwork to ensure your application is submitted accurately the first time. We handle the bureaucratic heavy lifting so you can focus on your life, knowing your paperwork is in professional hands. Frequently Asked Questions Will consolidating my loans lower my monthly payment? It can. Consolidation extends your repayment term up to 30 years, which lowers the monthly payment amount. Additionally, it allows you to apply for Income Driven Repayment plans that cap your payment at a percentage of your discretionary income. Does consolidation check my credit score? No. Federal student loan consolidation does not require a credit check. It is based entirely on your federal student loan balances. Can I undo a consolidation if I change my mind? No. Once a Direct Consolidation Loan is disbursed, the process cannot be reversed. This is why it is critical to understand the weighted average rules before you apply. Take Control of Your Student Loans Today The rules surrounding student loan forgiveness and consolidation have changed for the better, but they remain highly complex. You do not have to lose all your progress to achieve the simplicity of a single monthly payment. By understanding the weighted average rule, you can make an informed decision about your financial future. If you are tired of dealing with confusing servicer websites and want professional help preparing your consolidation and IDR applications, we are here for you. Get started with Docupop today. Let our document preparation experts ensure your paperwork is accurate, complete, and optimized for your specific repayment goals.

Getting married changes your federal student loan repayment options. Learn how tax filing status, income limits, and consolidation rules impact married borrowers.

Learn exactly how to consolidate federal student loans. Discover the step by step process, the pros and cons, and how to apply for lower monthly payments today

If you are staring at a monthly student loan bill that feels entirely out of touch with your actual income, you are not the only one. Millions of borrowers find themselves sacrificing basic living expenses just to keep their loans out of default. The standard 10-year repayment plan assigned to most federal student loans does not account for entry-level salaries, unexpected life events, or a rising cost of living. Fortunately, the Department of Education offers several avenues to reduce that monthly burden. The challenge is rarely a lack of options. The challenge is navigating the complex rules, applications, and consolidation requirements to secure the lowest possible payment. Here are the most effective, proven methods to lower your monthly student loan payments without relying on a temporary forbearance. Enroll in an Income-Driven Repayment (IDR) Plan For federal student loan borrowers, moving from the Standard Repayment Plan to an Income-Driven Repayment plan is often the fastest way to see a dramatic drop in monthly costs. IDR plans calculate your monthly payment based on your discretionary income and family size, rather than your total loan balance. If your income is low enough, your required payment could drop to $0 per month, while still keeping your loans in good standing. There are currently several IDR plans available, including: Saving on a Valuable Education (SAVE) Plan Income-Based Repayment (IBR) Pay As You Earn (PAYE) Income-Contingent Repayment (ICR) When applying for an IDR plan, you must recertify your income and family size annually. Failing to recertify on time will revert your payment to the standard amount. Because navigating which specific plan yields the lowest payment can be tedious, many borrowers utilize professional analysis to project their payments accurately before filing the paperwork. Consolidate Your Federal Student Loans Student loan consolidation involves combining multiple federal education loans into a single Direct Consolidation Loan. While consolidation itself does not inherently lower your interest rate, it does open the door to lower payments by extending your repayment term. Depending on your total loan balance, a Direct Consolidation Loan can extend your repayment period up to 30 years. A longer repayment term stretches the principal balance over more months, dropping the required monthly payment significantly. Consolidation also serves another vital purpose: it makes certain older loans, like FFEL or Perkins loans, eligible for modern Income-Driven Repayment plans and Public Service Loan Forgiveness. If your loans are currently in default, consolidation is also one of the primary pathways to rehabilitate the loans, remove the default status, and qualify for an income-based payment plan immediately. Pursue Public Service Loan Forgiveness (PSLF) If you work for a government agency or a qualifying not-for-profit organization, lowering your payments should be tied directly to a forgiveness strategy. The PSLF program forgives the remaining balance on your Direct Loans after you have made 120 qualifying monthly payments under an accepted repayment plan while working full-time for an eligible employer. To maximize the benefit of PSLF, borrowers should enroll in an IDR plan to keep their monthly payments as low as possible during that 10-year period. By paying the absolute minimum required based on income, you ensure the maximum amount of debt is left over to be forgiven tax-free at the end of the 120 months. Consider Extended or Graduated Repayment Plans If you do not qualify for an income-driven plan or prefer a fixed structure, the Department of Education offers two alternative structures. Extended Repayment: If you have more than $30,000 in outstanding Direct Loans, you can stretch your payments over 25 years. Payments can be fixed or graduated. Graduated Repayment: This plan starts with very low payments that increase every two years, assuming your income will grow over time. The loan is paid off within 10 years (or up to 30 years if consolidated). While these options lower your immediate monthly outflow, they do not offer a path to loan forgiveness. You will pay off the entirety of the debt, plus all the interest accrued over the extended timeline. Optimize Your Tax Filing Status Your tax filing status directly impacts how the government calculates your discretionary income for IDR plans. If you are married and file your taxes jointly, your student loan servicer will use your combined household income to calculate your monthly payment. This often results in a massive spike in your required payment. By choosing to file "Married Filing Separately," the servicer will typically only look at your individual income when calculating your monthly payment under plans like IBR or PAYE. While filing separately can cause you to lose certain tax deductions, the thousands of dollars saved on student loan payments over the course of a year often outweigh the lost tax benefits. Consulting with a loan expert or tax professional can help you run the math on both scenarios. Avoid Forbearance and Deferment Traps When borrowers cannot afford their payments, they often call their servicer and ask for a pause, known as forbearance or deferment. While this brings your payment to zero temporarily, it is not a long-term solution. During most periods of forbearance, interest continues to accrue and capitalize on your loan balance. When the pause ends, you will owe more than when you started, which can result in even higher payments. Instead of pausing payments, securing a $0 payment through an Income-Driven Repayment plan is a far better strategy. A $0 IDR payment counts toward loan forgiveness timelines, keeps your loans in good standing, and often includes interest subsidies that prevent your balance from ballooning. FAQ: Lowering Student Loan Payments Can I lower my student loan payments without refinancing? Yes. Federal student loan borrowers can lower their payments without private refinancing by enrolling in Income-Driven Repayment plans, extending their repayment terms through consolidation, or qualifying for targeted forgiveness programs. Does consolidating student loans lower the monthly payment? Consolidating federal loans can lower your monthly payment by extending the repayment term up to 30 years. It also simplifies your debt into one single monthly bill. What happens if my income drops while on an IDR plan? If your income drops or you lose your job, you do not have to wait for your annual recertification date. You can request an immediate recalculation of your IDR payment based on your current financial situation. Take Control of Your Repayment Strategy There is no single "best" way to handle student debt. The ideal strategy depends entirely on your loan types, income trajectory, family size, and career path. Trying to guess which federal program yields the lowest payment can result in years of overpaying or missed forgiveness opportunities. At Docupop, our team of experienced student loan coaches specializes in cutting through the confusion. We provide a comprehensive loan analysis to identify exactly which programs you qualify for, map out your potential savings, and handle the heavy lifting of document preparation so you know it is done right. Speak to a Student Loan Expert at No Cost and discover how much you could lower your monthly payment today.

Millions of Americans carry federal student loan debt. For many borrowers, managing that debt feels like a part time job. You might have loans split between different servicers, multiple due dates, and varying interest rates. You might also be trying to figure out if you qualify for Income Driven Repayment or Public Service Loan Forgiveness. Federal student loan consolidation is often the first step to taking control of your educational debt. Consolidating your loans can simplify your monthly payments, open the door to better repayment plans, and help you get out of default. However, the rules surrounding federal student loans change frequently. Filing the wrong paperwork or misunderstanding the terms of your consolidation can cost you time and money. This guide explains exactly how federal student loan consolidation works, the benefits and drawbacks, and how to ensure your documents are prepared correctly. What is a Direct Consolidation Loan? A Direct Consolidation Loan allows you to combine multiple federal student loans into a single new loan backed by the United States Department of Education. When you consolidate, the government pays off your existing loans and issues you a new one. This new loan will have a single monthly payment and a single fixed interest rate. The new interest rate is the weighted average of the interest rates on your previous loans, rounded up to the nearest one eighth of a percent. It is important to understand that federal consolidation does not lower your interest rate. If your goal is strictly to secure a lower interest rate, you would need to look into private refinancing. However, private refinancing strips away all federal protections. Federal consolidation keeps your loans in the federal system, preserving your access to government forgiveness programs and flexible repayment options. The Strategic Benefits of Consolidating Federal Loans Borrowers do not consolidate federal loans to save on interest. They consolidate to gain access to better administrative options and federal protections. Here are the primary reasons you should consider consolidating your federal student debt. Accessing Income Driven Repayment Plans Income Driven Repayment plans base your monthly payment on your income and family size rather than your total loan balance. If your income drops, your payment drops. After a set period of years, usually 20 or 25, any remaining balance is forgiven. Not all federal loans qualify for these plans automatically. For example, older Federal Family Education Loan Program loans or Perkins Loans often need to be consolidated into a Direct Consolidation Loan before they become eligible for the most beneficial Income Driven Repayment options. Qualifying for Public Service Loan Forgiveness The Public Service Loan Forgiveness program forgives the remaining balance on your Direct Loans after you have made 120 qualifying monthly payments under an accepted repayment plan while working full time for a qualifying employer. Qualifying employers include government organizations and tax exempt non profits. Only Direct Loans are eligible for this program. If you have older loan types, you must consolidate them into a Direct Consolidation Loan to participate. Ensuring your paperwork is flawless here is critical. A single missed detail on an employment certification or consolidation application can delay your progress by months. Getting Out of Default If you have fallen behind on your student loans and entered default, the consequences are severe. The government can garnish your wages, withhold your tax refunds, and damage your credit score. Consolidating your defaulted federal student loans is one of the fastest ways to get back into good standing. To do this, you must agree to repay the new Direct Consolidation Loan under an Income Driven Repayment plan, or you must make three consecutive, voluntary, on time, full monthly payments on the defaulted loan before you consolidate. Once the consolidation is processed, the default status is removed from your active record. Potential Drawbacks You Need to Understand While consolidation is highly beneficial for many, it is not a perfect solution for everyone. You need to weigh the potential downsides before you submit any applications. Capitalization of Unpaid Interest When you consolidate, any unpaid interest on your existing loans is capitalized. This means the outstanding interest is added to your principal balance. Your new loan will generate interest based on this higher principal amount. Over the life of the loan, this can result in paying more total money. Losing Progress on Forgiveness Timelines Historically, consolidating your loans meant resetting the clock on any progress you had made toward Income Driven Repayment forgiveness or Public Service Loan Forgiveness. The Department of Education has occasionally issued temporary waivers to adjust these rules, but the baseline regulation states that a new consolidation loan is a brand new loan with zero qualifying payments. You must be completely sure of the current Department of Education guidelines before you consolidate if you are close to the finish line for forgiveness. Extending the Repayment Term Consolidation gives you a new repayment term that can last up to 30 years. While spreading your payments out over a longer period will lower your monthly bill, it also means you will be in debt longer and will pay more interest over time. You can offset this by choosing an Income Driven Repayment plan or paying more than the minimum each month. Federal vs. Private Consolidation Borrowers frequently confuse federal consolidation with private student loan refinancing. They are completely different financial maneuvers. Federal consolidation combines only federal loans. It is managed by the Department of Education. It does not require a credit check. It keeps your loans eligible for federal forbearance, deferment, and forgiveness. Private refinancing involves a private bank or online lender paying off your federal loans and issuing you a new private loan. This requires a credit check. It can result in a lower interest rate if you have excellent credit. However, once you refinance federal loans with a private lender, they are gone from the federal system forever. You permanently lose access to Income Driven Repayment, Public Service Loan Forgiveness, and administrative forbearance. If you anticipate ever needing flexible payments based on your income, or if you work in public service, you should keep your loans in the federal system. Why Borrowers Struggle with the Process Applying for federal loan consolidation is free through the Department of Education. So why do so many borrowers struggle with the process? The application process is dense. You have to gather loan codes, verify servicer details, and choose the correct repayment plan from a confusing list of options. If you select the wrong repayment plan during consolidation, your monthly payment could jump drastically. Furthermore, loan servicers are notorious for providing conflicting information. Over the last few years, millions of accounts have been transferred between companies like FedLoan, Navient, MOHELA, and Nelnet. These transfers have resulted in lost paperwork, miscalculated payment counts, and customer service gridlock. When you call a servicer for help, you may wait on hold for hours only to speak with a representative who gives you incorrect advice. The burden of getting the paperwork right falls entirely on the borrower. If you submit an incomplete form, the government will simply reject it, delaying your access to lower payments. How Docupop Simplifies the Process This is where Docupop steps in. Think of the student loan system like the tax system. Anyone can file their taxes for free using IRS forms. Yet millions of people pay CPAs and tax software companies every year to handle the process for them. They do this to save time, avoid critical errors, and ensure they are utilizing every rule to their advantage. Docupop is a document preparation service specifically designed for federal student loan borrowers. We do not lend money, and we do not buy your loans. We manage the bureaucracy. When you use Docupop, our team evaluates your specific financial situation, your loan types, and your career path. We prepare your federal consolidation and Income Driven Repayment applications with total accuracy. We track the documents, handle the administrative heavy lifting, and ensure that your paperwork is submitted exactly as the Department of Education requires. You can navigate the federal student loan system alone. But if you are tired of confusing paperwork, frustrated by servicer call centers, and worried about making a costly mistake, Docupop offers a clear path forward. Frequently Asked Questions Does consolidating my federal student loans lower my interest rate? No. Your new interest rate will be a weighted average of your previous federal loan interest rates, rounded up to the nearest one eighth of a percent. The goal of federal consolidation is to simplify payments and qualify for federal programs, not to secure a lower rate. Can I consolidate my federal and private student loans together? You cannot combine private and federal loans into a Direct Consolidation Loan. Federal consolidation is strictly for loans issued by the federal government. If you want to combine both types, you would have to use a private lender, which means losing all your federal protections. How much does it cost to consolidate federal student loans? There is no fee to apply for a Direct Consolidation Loan through the Department of Education at StudentAid.gov. If you choose to hire a document preparation company like Docupop to handle the paperwork, analyze your options, and manage the filing process, you will pay a service fee to that company for their expertise and time. Will consolidation affect my credit score? Consolidating your federal loans does not require a credit check, so there is no hard inquiry on your credit report. However, your credit score may fluctuate slightly because older loan accounts will be closed and a new loan account will be opened, which can temporarily affect your average age of credit history. Take Control of Your Student Loans Today Ignoring your student loans will not make them disappear, and waiting for your loan servicer to offer helpful advice is a losing strategy. The rules are complex, the paperwork is dense, and the cost of making a mistake is high. You have options to lower your payments, get out of default, and position yourself for forgiveness. You just need to make sure the process is handled correctly. If you are ready to take control of your financial future without dealing with the stress of government paperwork, we are here to help. Docupop handles the document preparation so you can have peace of mind. Visit our consolidate.docupop.com to learn how our experts can prepare your federal student loan consolidation applications accurately and efficiently.

New PSLF rules in 2025 may limit student loan forgiveness. Learn how to protect your eligibility and what steps to take now to stay on track.

Trump’s Big Beautiful Bill could reshape student loans. Discover 8 major changes coming to repayment, forgiveness, PLUS loans, and IDR plans in 2025.

Got Parent PLUS Loans? Discover your options for forgiveness and repayment in 2025, including how to lower payments through consolidation and qualify for relief.